Carve-Out:

Boosting corporate value

through professional carve-out management

„Companies often revert to carve-outs to improve their competitive position and boost company value. While carve-outs are not the most glamorous corporate transactions, they are among the most complex. Yet, masterfully prepared and executed, they increase the value of the parent and the divested company. EIP interim managers focus solely on creating value and possess all skills to lead carve-outs to success.“

Markus Nicolaus, Partner, Executive Interim Partners GmbH

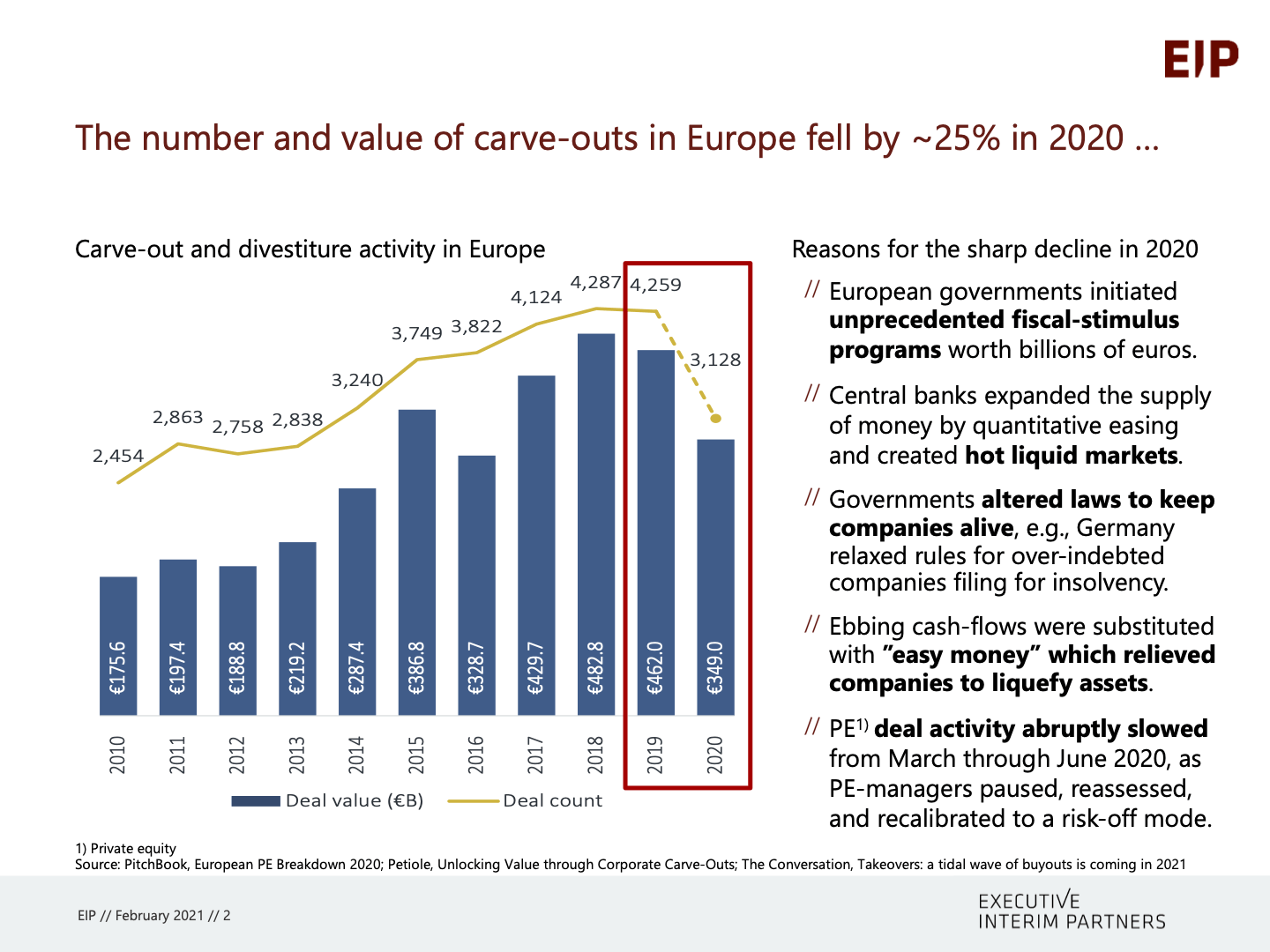

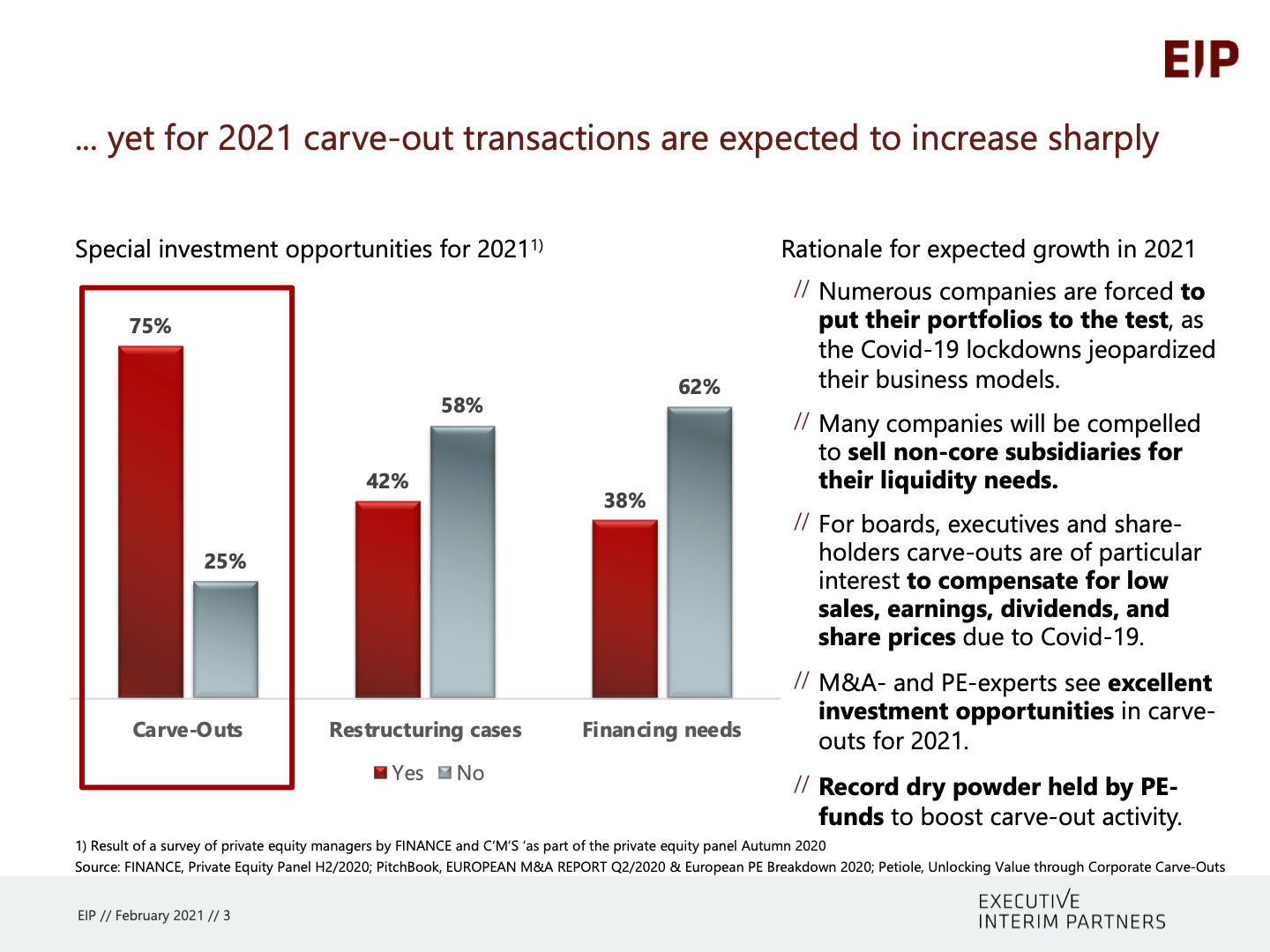

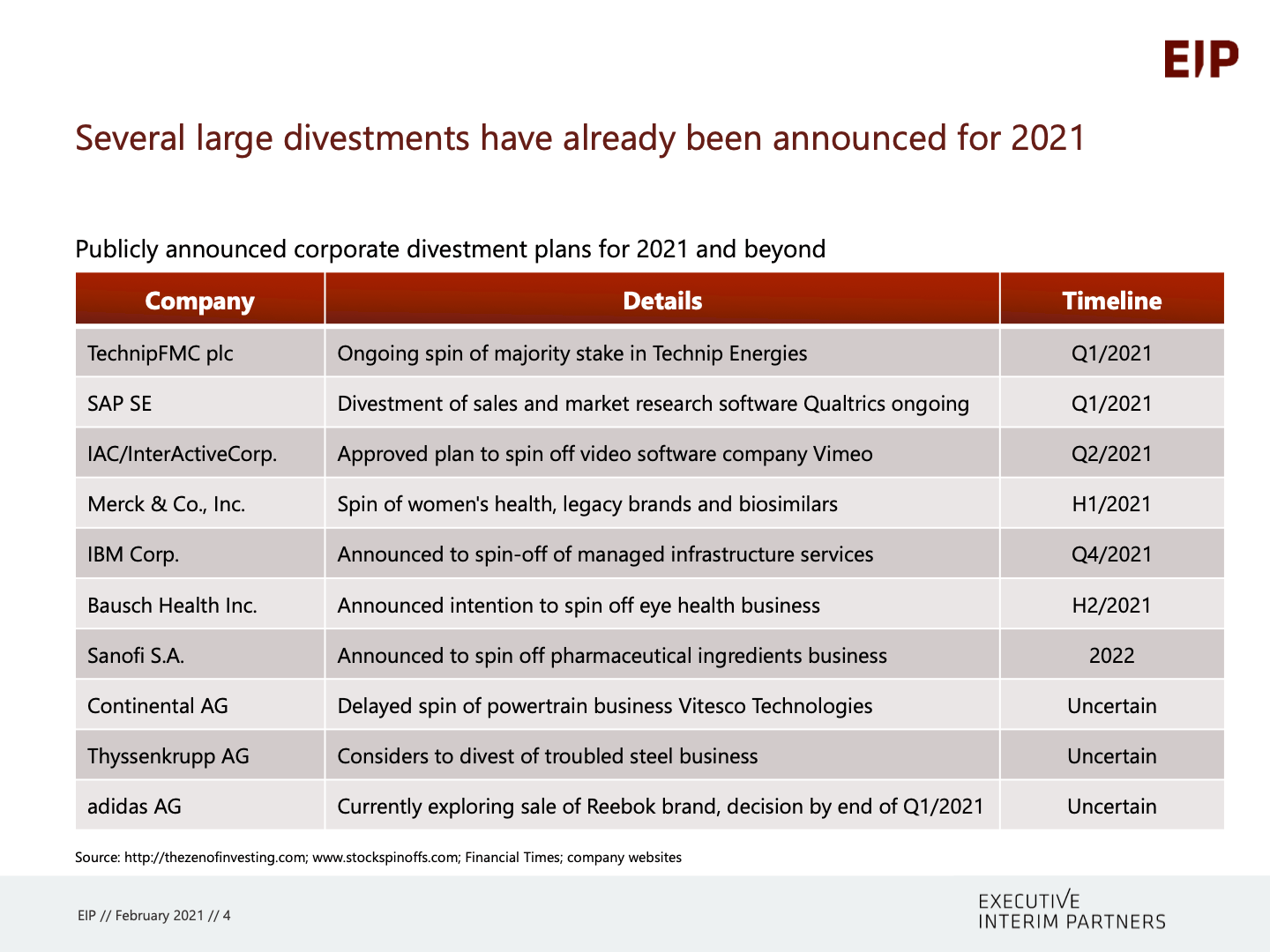

M&A experts anticipate that numerous corporations, forced or motivated by the Corona crisis’s economic impact, will put their business model and portfolios to the test in the coming months. The private equity community shares this assessment, which is why 75% of the panel participants in the FINANCE Private Equity Panel Q2/2020 see excellent investment opportunities in carved-out assets for 2021. In Europe, record dry powder held by private equity funds is forecasted to boost carve-out activity in 2021. The finance information service PitchBook also expects carve-out activity to pick up quickly this year as public and private companies seek to offload non-performing assets to raise liquidity amid the pandemic turmoil. US companies are facing a similar situation, which can put more pressure on them to sell non-core assets. As desired, these carve-outs will serve to generate capital from assets to compensate for the falling cash flows from the decline in sales in the recent months and in particular, to increase corporate values.

Do you want to have the carve-out of your company designed by professionals? Then contact us now and learn more about us and our approach.

Carve-outs, spin-offs and split-offs are different transactions that companies typically use to divest of certain assets such as business units, subsidiaries and other company parts. The objective of these transactions is usually to increase the enterprise value of the parent corporation and the carved-out company.

In a carve-out event, the parent company sells the asset either directly to a strategic investor or financial investor or indirectly to several investors as part of an IPO. Through the sale the investors become new (co-)owners of the carved-out company. Simultaneously, the parent company receives additional financial resources, often one of the primary motivations for this transaction.

In the case of a spin-off, a listed parent company distributes the shares in a spun-off subsidiary proportionally to its previous shareholders in the form of a special dividend. After the spin-off, the shareholders hold the shares of two separate companies. However, the parent company does not receive any cash from the spin-off. The same applies to the split-off. The parent company shareholders have to decide whether to hold shares in the subsidiary or continue to keep those of the parent company.

They are thus more likely to focus on long-term strategic objectives to increase the company’s value successfully. This also applies, if the funds derived from the carve-out are invested in the parent’s company strategic growth and not just used for mere survival. Regardless of whether the carve-out intends to serve strategic development or improve its financial position, the company executive management asks how the carve-out will achieve a maximum cash inflow for the parent company.

Carve-outs are incredibly complex transactions that require meticulous planning and excellent execution to be successful. The carve-out’s professional preparation and implementation typically have a very positive effect on the targeted sales price.

The results of a survey of 150 executives who are regularly involved in corporate divestments show that in 85% of the cases the sales price achieved matched or even exceeded the seller’s expectations. The particularly beneficial factors were:

In particular, the scope and reliability of the information provided about the company’s part considered for divestment and well-prepared management promote the confidence of potential buyers in the carve-out property’s intrinsic and stable value. As a result, the potential buyers typically apply lower risk discounts on the enterprise value and the purchase price. These factors also promote trouble-free negotiations between buyers and sellers, which lead to a faster conclusion of a contract for the sale. For most corporations and their management, the sale of parts of the company is a unique situation. Executive leadership has to figure out how the intended carve-out can be carefully planned and professionally prepared to achieve a swift sale with the desired success.

In principle, we can divide carve-outs into four phases

In the design phase, the most critical parameters for the carve-out need to be determined and defined. Additionally, to identify the carve-out object (NewCo), the rationale for the planned divestiture and which carve-out approach and timeframe the sale and the carve-out need to complete is defined. Furthermore, identifying potential buyers, the preferred sales strategy, and necessary project guidelines are defined. As another essential part of the design phase, the rough concept for the company’s future business model and the appropriate transfer process for NewCo are also defined. In addition to setting up a project organization, that is still lean at first, assigning responsibilities and selecting external service providers, it is recommended to appoint a carve-out executive manager and establish a dedicated carve-out management office (CMO). The carve-out executive works closely with the M&A team and instills his extensive operational carve-out experience across all phases of the entire carve-out transaction.

in the preparation phase, a multitude of activities takes place before potential buyers are contacted. The most critical tasks in preparing for a successful carve-out include:

The parent company’s management must have clarity as to what is to be carved out and sold in concrete terms. We can quickly identify it in the case of a subsidiary that operates 100% independently and with which there are no extensive operational, personnel, financial or legal links. It becomes challenging when there are close ties and dependencies between the parent company and the carve-out property. Often parts of the company use the same IT, HR, procurement, finance and controlling infrastructure as well as a variety of other resources from the central functions of the parent company. Usually, the same applies to real estate, patents, rights of use, suppliers, customers, service providers, employees, etc. For the clear definition of the company part planned to be carved out, it must be specified in detail what is part of the carve-out scope and what will remain with the parent company. Finally, the buyer also wants to know what he is acquiring by purchasing the carve-out object.

Regularly there are no or only insufficient financial data and reports available of the company part being divested. The same applies to financial analyses, which potential buyers urgently need to make their calculations on the company’s profitability and enterprise value. This is due to the fact that the carve-out object is often not an independent business with corresponding reporting obligations. Furthermore, there are often allocations and intercompany settlements of the parent company for centrally provided services, which usually do not correspond to market prices. Comprehensive and reliable historical financial reports and analyses must be prepared with auditors and other consultants’ help.

For a successful sale, a separate stand-alone business planning of the company’s part to be carved out is indispensable. This should preferably be created with potential buyers in mind and consider potentials in the market, competitors, customers, suppliers and other synergies. Business planning must also reflect that there will no longer be any links and dependencies with the parent company in the future. Contrary to planning for purely internal purposes, a particular challenge is that potential buyers have high expectations regarding the stand-alone business planning reliability. If these expectations are not met, trust in the seller’s credibility decreases, the sales process gets delayed and the sales price typically decreases. Against this background, the stand-alone business planning for the next three to five financial years becomes a highly complex challenge, which can often not be mastered without independent professional service providers’ active support.

The business planning created is also used as a basis for valuation of the carve-out property from a seller’s point of view. Using different scenarios and valuation methods such as discounted cash flows, EBITDA or sales multiples, etc. the carve-out property’s value is usually calculated with the support of M&A consultants. For the first time, the parent company receives a well-founded indicator of a possible sales price for the carve-out property.

With careful carve-out planning, the carve-outs property transfer from the current state to the future business model or the target state is mapped out. The aim is to eliminate any potential or existing ambiguities and create transparency on the operational procedure, the resources required, the costs incurred, the investments needed and the timeframe for the implementation of the carve-out. Also, business furthermore needs transition service agreements (TSA) during the transitional period until the complete decoupling from the parent company is completed. Before these measures and other preparatory activities for the operational carve-out, the project team must be named, the project organization to be set up and the necessary communication rules to be established. The carve-out executive is primarily responsible for these tasks getting hands-on support from the carve-out management office (CMO).

Do you want to have the carve-out of your company designed by professionals? Then contact us now and learn more about us and our approach.

The implementation phase begins with the conclusion of the contract (signing) between buyer and seller. This is when the operational implementation of the carve-out usually begins. In this phase, it is essential to implement all steps of the detailed carve-out planning. As a rule, all parent company employees and the company’s part to be carve-out are informed about the sale and the carve-out at the time of signing. To keep the employees involved, and motivated, the messages concerning the sale and carve-out must be carefully prepared and communicated. Measures and incentives to secure high motivation of all performers involved are usually prepared and, if necessary, communicated already early in the carve-out preparation phase. Such measures should now also be considered for other employees depending on the situation. Transparent communication on the purpose and benefits of the carve-out and showing opportunities for future personal development and perspectives are significant important measures in this context.

If not already done during the preparation phase, the transition service agreements’ content must be drawn up and negotiated in detail with the buyer. The parent company must take appropriate precautionary measures to effectively provide the agreed services after the operational carve-out has been completed.

In preparation for the final handover of the carve-out property, a “Day-1 Readiness Check” must be carried out well in advance. The check verifies whether all areas are adequately prepared for Day-1 or Go-Live. The review includes, among other things, all TSA, the necessary communication with suppliers, customers, service providers, public bodies, banks and other business partners as well as the testing of the IT infrastructure and applications. The “Day-1 Readiness Check” often brings up unexpected challenges that can usually still be eliminated due to sufficient lead time and with a focused approach.

The handover (cut-over) for Day-1 or Go-Live must be planned in detail. However, due to changing framework conditions, unexpectedly arising new challenges, eventualities and circumstances, necessary deviations from the original cut-over planning may occur. In such cases, quick and precise decisions on how to proceed are essential for carve-out success. This is where the carve-out executive proves his worth. He/She usually takes the necessary decisions himself promptly and, with the CMO’s support, can also evaluate their effects on the entire carve-out.

The post-closing phase starts with Day-1 or Go-Live, with which the operational carve-out is mostly completed. The parent company essentially ends the project work after the carve-out transaction has been completed. However, for a short period following the completion, it is advisable to maintain access to the project team and have the CMO still available for coordinating activities. Experience has shown that unexpected challenges arise in the weeks after the Go-Live, which have to be mastered quickly in the sense of a “trouble-shooting”. Here access to the carve-out executive, the CMO and the project team is usually beneficial. The carve-out executive and the CMO should also continue to be involved in the knowledge transfer to optimize the parent company’s business and in monitoring the smooth start and the quality of the TSA provision.

Carve-Outs are a veritable unique situation for companies. They demand skills, experience, and expertise from management and employees that go far beyond managing day-to-day business. Even minor discrepancies can lead to a loss of confidence among potential buyers and small delays can lead to the postponement of the carve-out. At worst, such events even lead to the cancellation of the entire carve-out.

In addition to the conditions and parameters described above, the following framework conditions and measures are critical factors for successful carve-out transactions:

Executive management can actively increase the value and improve the financial position of their respective company through divesting assets in carve-out transactions. In addition to extensive carve-out experience, these transactions’ extraordinary complexity requires professional carve-out management skills to achieve a high sales prices from the divestment and an uninterrupted, trouble-free separation from the parent company. An experienced carve-out executive backed by a strong operational carve-out management office (CMO) supports or even frees up company executive management from the time consuming carve-out preparation as well as execution. Thus, sufficient room to maneuver for executive management and company staff is created to fully focus on the core business of the parent company, unlock untapped potential and spur further profitable growth. Equally, the top management and staff of NewCo get sufficient leeway to focus on establishing the new company in the market successfully. Our EIP interim managers focus solely on creating value and possess all skills needed to lead carve-outs to success, for the parent corporation and the carved-out entity.

Read the full article by Markus Nicolaus here:

We will get back to you as soon as possible

Do not hesitate and let us advise you – discretion is guaranteed

Under normal circumstances, the executive management or the board of directors decides to divest of a part of the company because it no longer fits the company's core business. The carve-out creates the opportunity to focus entirely on the core business and thus to sustainably increase the company's value. This applies to both the parent company and the carve-out property. The parent company then often uses the funds obtained from the sale for its own business operations or uses them to purchase new business activities or assets of other companies.

In a crisis, i.e. a special situation for the company, the executive management or the board of directors usually intends to generate additional financial resources by selling parts of the company and thus to ensure the survival of the parent company. For example, the sales proceeds can be used to compensate for falling cash flows from declining sales. The company remains liquid and an impending bankruptcy can be averted. In addition, crises usually mean that companies have to strategically realign themselves in the market in order to be successful in the long term. The realignment means that certain business activities will no longer be part of the company's core business in the future. As part of a portfolio streamlining, these business activities are then divested of.

Carve-outs are planned, prepared and implemented in parallel to the typical day-to-day operations of a company. This alone is a severe additional workload for the executive management and employees of the company, which often becomes an ordeal. Sufficient employees, with the adequate capacity and appropriate know-how must be available, to successfully carry out the carve-out alongside day-to-day operations. Since carve-outs are typically special situations, the methodical knowledge for a carve-out within the company is usually not available at all or only in rudimentary form. It is therefore advisable to hire an experienced carve-out executive temporarily, who is operationally supported by a professional carve-out management office (CMO). The carve-out executive typically develops and establishes the entire project organization, controls decisions critical to success, e.g. on the IT environment or IT systems, monitors the creation of employee transfer and retention plans as well as the drafting of transition service agreements (TSA), among other things.

Residenzstraße 27

Preysing Palais

80333 Munich

Phone: +49 89 552 7979 20

Fax: +49 89 552 7979 01

© Copyright – Executive Interim Partners

{kind=link}

{kind=link}

{kind=link}